7 Mistakes You’re Making With QuickBooks Automation

It’s June, and if you’re anything like me, you’d rather be literally anywhere else than staring at a laptop screen. Here in Anchorage, the sun is high, the fish are biting, and the last thing you want to do is spend your Saturday afternoon arguing with a bank feed.

That’s why we love automation, right? It’s the "easy button" for business owners. You click a few boxes, set a few rules, and suddenly, you’re a "tech-savvy entrepreneur" instead of a person drowning in receipts.

But here’s the cold, hard truth: QuickBooks Online (QBO) automation is a double-edged sword.

When it works, it’s a lifeline. When it’s set up wrong? It’s a slow, helpless slide toward financial failure. I’ve seen books that would make your eyes bleed, not because the owner was lazy, but because they trusted the software too much. They thought they were "automating" their success, but they were actually automating a disaster.

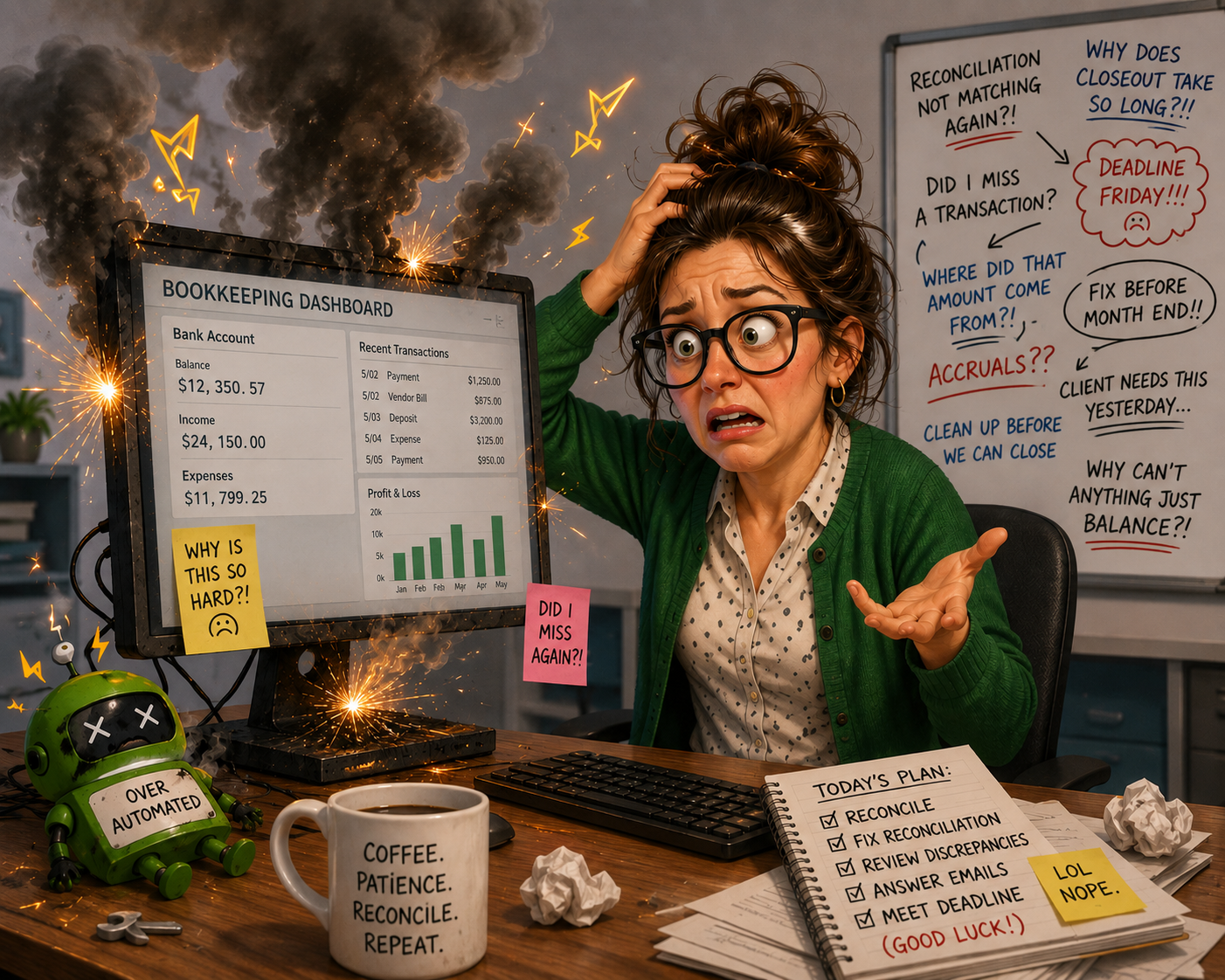

If you’re feeling like your reports don't match the reality of your bank account, you might be making one of these seven common mistakes.

1. The "Auto-Add" Bank Rule Trap

We’ve all seen that tempting little checkbox in the bank rules: "Automatically add to my books."

It sounds like a dream. You tell QBO that every time it sees "Chevron," it should categorize it as "Fuel." You check the "Auto-add" box, and boom, it’s done. You never have to look at it again.

The Problem: Automation has zero common sense. If you buy a bag of chips and a car wash at Chevron, it’s "Fuel." If you buy a new set of tires at a shop that somehow gets flagged with the same keyword? It’s "Fuel."

When you turn on "Auto-add," you are essentially abdicating your responsibility to review your spending. I’ve seen owners "auto-add" thousands of dollars into the wrong categories for months before realizing their Profit & Loss report was a work of fiction.

The Solution: Turn off "Auto-add." Period. Use rules to suggest a category, but make yourself click "Add" manually. It takes five seconds, but it saves you five hours of cleanup later.

2. "Adding" Instead of "Matching"

This is the single most common way small business owners accidentally inflate their income (and their tax bill).

Imagine you send an invoice to a client for $1,000. They pay you. You record that payment in QBO. Great! Now, a few days later, that $1,000 hits your bank feed. QBO shows a "Match" button, but you’re moving fast, and you just click "Add."

The Agitation: You just told QuickBooks you made $2,000. You have the $1,000 from your invoice and a new $1,000 from the bank feed. You are now paying taxes on money that doesn't exist.

The Solution: Always, always, always look for the green "Match" icon. If it’s not there, ask yourself why. Did you forget to record the payment? Is there a discrepancy in the amount? Never click "Add" if you’ve already created a transaction for that money elsewhere.

3. The "App-Sync" Double Dip

I love a good integration. Shopify, Square, Stripe, they make life easier. But they are also the primary suspects in the Case of the Messy Books.

A common scenario: Your Square app is synced to QBO. Every day, it pushes a "Sales Receipt" into your books. Then, your bank feed shows a deposit from Square. If you "Add" that bank deposit as "Sales," you have doubled your income.

The Game Changer: You need to decide which system is the "Source of Truth." If your app is recording the sales, your bank feed should only be matching those sales or hitting a "clearing account." If you don’t understand how your apps are talking to QBO, you’re basically flying a plane with a broken compass.

4. Treating Transfers Like Expenses

QuickBooks is smart, but it’s not a mind reader.

When you pay your business credit card from your business checking account, that is not an "Expense." It’s a Transfer. When you take $500 out for a personal "Owner’s Draw," that is not an "Expense." It’s an Equity move.

If your automation rules are set to categorize every "transfer" as "Office Supplies" or "Miscellaneous," your balance sheet is going to look like a crime scene. You’ll be "losing" money on paper that is actually just moving between your own pockets.

Action Item: Check your "Transfers" once a month. If they are landing in your P&L (Profit & Loss) instead of your Balance Sheet, you’ve got a leak in your logic.

5. Thinking "Automated" Means "Reconciled"

I’m going to say this loudly for the people in the back: Categorizing transactions in the bank feed is NOT the same thing as reconciling.

I’ve had clients tell me, "My books are done! I’ve cleared the bank feed every day!" Then I look at their reconciliation screen and see they haven't actually reconciled the account in three years.

The Reality: Automation can miss things. Banks can have glitches. Duplicate entries happen. Reconciliation is the "fail-safe" that ensures the number in QuickBooks actually matches the number on your bank statement. If you aren't reconciling monthly, you are essentially guessing. And guessing is a great way to end up with a surprise tax bill or a bounced check.

(Need a hand getting back on track? Check out why your small business needs a QBO Optimization to fix these exact issues.)

6. Messy Sales Tax Mappings

If you use automation to record sales, you better be 100% sure the sales tax is mapping correctly.

Many apps will push the total deposit into QuickBooks as one lump sum. If that $100 deposit includes $8 of sales tax, and you record the whole $100 as "Income," you are overstating your revenue and understating your liabilities.

When it comes time to pay the state, you’ll be scrambling to find the money because it’s already been "spent" or accounted for as profit. This is how small businesses get into hot water with the tax man, and trust me, nobody wants that stress.

7. Leaving the "Back Door" Open

Did you know that an automated app or a poorly written bank rule can actually change your data from last year?

If you haven’t "Locked" your books after filing your taxes, a sync error today could reach back into December 2025 and change a transaction. Suddenly, your tax return and your books don’t match anymore.

The Fix: Use the "Close the Books" feature in QBO. Once a month is over and reconciled, lock it with a password. This prevents your automation from "fixing" things that aren't broken.

The Bottom Line: Automation Needs an Architect

QuickBooks Online is a powerful tool, but it’s just that, a tool. It’s like a high-end power saw. In the hands of a pro, it builds a house. In the hands of someone who isn't paying attention, it... well, it causes a lot of blood and a trip to the ER.

As a QuickBooks Online Pro, I’ve spent years helping business owners who got trapped in the "set it and forget it" mindset. They wanted to save time, but they ended up losing money and peace of mind.

Are you worried your automation is working against you?

Don't let the stress of "what if" ruin your summer. I specialize in QBO Optimization and Diagnostics. I can go in, clean up the mess, fix your rules, and give you a fresh start.

You deserve to know your numbers are right. You deserve to work with someone who’s been in your shoes and understands that bookkeeping isn't just about math: it's about the survival of your business.

Ready to stop fighting the software and start growing your business?

Let’s talk. Whether you have a quick question or need a full-scale cleanup, I’m here to help you get back to what you do best.